The dual interface card — a single card that supports both contact (chip-and-PIN) and contactless (tap-to-pay) transactions — has rapidly become the standard specification for new banking card issuances worldwide. For African banks upgrading their card portfolios, dual interface represents the optimal investment: a single card that works in every possible transaction scenario, from a chip reader at a traditional point-of-sale terminal to a contactless tap at a modern payment device.

One Chip, Two Interfaces

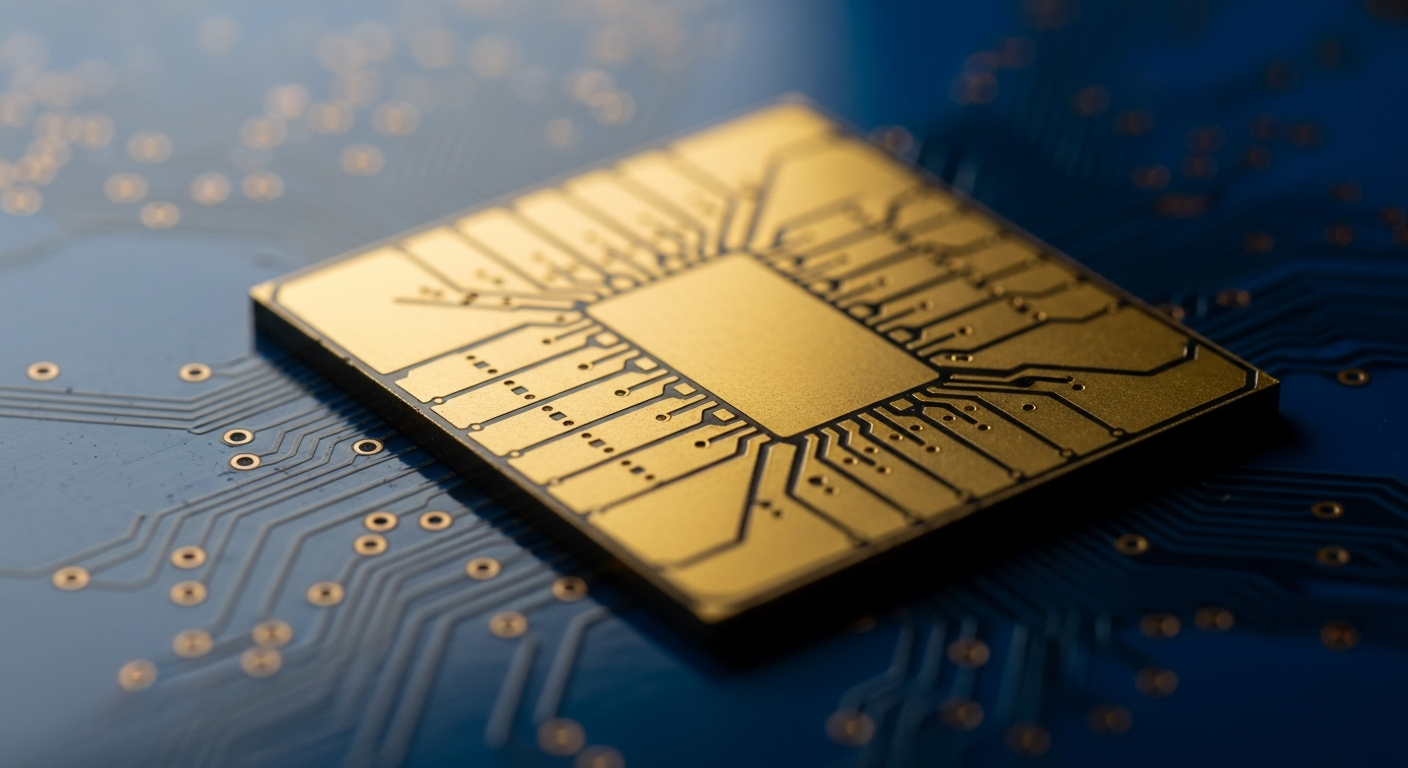

At the heart of a dual interface card is a single microprocessor chip that communicates through two distinct channels. The contact interface uses the familiar gold-plated contact pad on the card's surface, making direct electrical connection with a card reader when the card is inserted. The contactless interface uses an antenna coil embedded within the card body, communicating wirelessly with NFC readers at 13.56 MHz.

Both interfaces connect to the same chip, which runs the same payment application and stores the same credentials. Whether a transaction is initiated via contact or contactless, the cryptographic processing, cardholder verification, and transaction authorisation follow the same EMV protocols. The difference is purely in the physical communication layer — the logic and security are identical.

This shared architecture is elegant but technically demanding. The chip must be designed to switch seamlessly between power sources — drawing current from the reader via the contact pads in one mode, and harvesting energy from the reader's electromagnetic field via the antenna in the other. The chip's firmware must manage both communication protocols simultaneously, and the card's antenna must be precisely tuned to deliver reliable contactless performance without interfering with the contact interface.

The Manufacturing Challenge

Producing a dual interface card is significantly more complex than manufacturing either a contact-only or contactless-only card. The process begins with the card body — multiple layers of PVC or composite material that are laminated together under heat and pressure. For a dual interface card, the antenna must be embedded between these layers with extreme precision.

The antenna is typically a flat coil of fine copper or aluminium wire, wound in a specific pattern that is optimised for the card's target operating frequency and the characteristics of the chip module being used. The number of turns, the wire gauge, the spacing between turns, and the overall dimensions of the coil all affect the card's RF performance — its read range, coupling efficiency, and susceptibility to interference.

The most critical manufacturing step is the connection between the chip module and the antenna. In older dual interface card designs, this connection was made using conductive epoxy or wire bonding, which could be fragile and prone to failure. Modern production techniques use hot-lamination coupling or laser bonding to create robust, permanent connections that withstand the mechanical stresses of card usage — bending, flexing, and the impact of being dropped or sat upon.

Chip Platform Selection

The choice of chip platform for a dual interface card is driven by the payment application requirements, the issuing bank's preferences, and the certification requirements of the payment networks. The major chip suppliers — Infineon, NXP, Samsung, and STMicroelectronics — all offer dual interface chip modules that have been pre-certified by Visa, Mastercard, and other networks.

Common platforms include the Infineon SLE78 family, widely used in European and African banking card programmes; the NXP SmartMX series, favoured in the transit and multi-application segment; and various offerings from Samsung and ST that compete on price and performance. Each platform has its own characteristics in terms of processing speed, memory capacity, cryptographic algorithm support, and power consumption — the last being particularly important for contactless operation, where the chip must function on the limited energy harvested from the reader's RF field.

The Business Case for Issuers

Dual interface cards cost more to manufacture than contact-only cards — typically 30 to 50 per cent more, depending on the chip platform and production volume. This cost premium has historically been a barrier to adoption, particularly in cost-sensitive African markets. However, the economics are shifting in favour of dual interface for several reasons.

First, contactless transaction limits have been raised across most African markets, increasing the utility of the contactless interface. Second, the operational cost savings from contactless — faster transaction times, reduced terminal wear, and fewer card insertions that can damage contact pads — offset the higher card cost over the card's lifecycle. Third, consumer demand for contactless is growing, and banks that issue contact-only cards risk appearing technologically behind their competitors.

Finally, the argument for future-proofing is compelling. A dual interface card issued today will function correctly whether the cardholder uses it in a chip-and-PIN terminal, a contactless payment terminal, or an ATM. A contact-only card, by contrast, cannot access the growing number of merchant locations that offer only contactless acceptance — a scenario that is becoming increasingly common in developed markets and will eventually emerge in Africa.

Quality Is Non-Negotiable

The complexity of dual interface card manufacturing places extraordinary demands on quality control. Every card must undergo RF testing to verify contactless performance, contact interface testing to confirm chip communication, and physical stress testing to ensure the antenna connection withstands real-world use. At Cardzgroup, our production teams employ automated testing equipment that validates every dual interface card before it leaves the factory, ensuring that our clients receive cards that perform flawlessly from first tap to last.